FAQ

-

Who we are?

Transferty is a payment gateway provider that proposes payment processing solutions for businesses of all sizes. Our first product is an all-in-one payment gateway developed to optimize your flow and maximize conversion. A white-label payment gateway is our second product aimed at covering the needs of those who are looking for a reliable and effective solution under their own brand. We are fintech enthusiasts with a clear vision of how global payments should perform to satisfy the needs of leading companies, big enterprises, and merchants aiming to grow globally

-

Can Transferty open MIDs for clients?

No. Each client is able to open MIDs according to the specific needs of the business and then integrate them into the Transferty payment gateway. To get a merchant account number, or MID, you have to sign an agreement with an acquiring bank, or PSP

-

Do we store the customer’s funds?

No, we do not handle the actual transfer of funds. As a payment gateway, our main role is to facilitate the transmission of technical information related to a customer’s payment request. This information includes details such as the customer’s card information and the merchant they wish to pay. We securely transmit this information to the payment service provider (PSP) or bank-acquirer who then interfaces with the relevant financial institutions involved. The responsibility for the transfer of funds lies with the bank-acquirer, card networks (e.g., Visa, Mastercard), and the customer’s bank issuer. Our focus is solely on securely transmitting the payment data and ensuring a smooth transaction process, without directly handling or holding any funds

-

Who are our clients?

Our products are developed to fit the requirements of all sizes of businesses, including SMEs as well as large enterprises and industry leaders. Transferty’s payment gateway aims to satisfy all the needs of merchants globally. Our white-label payment gateway can be customized for each client’s individual needs. It is available for enterprises as well as each business that wants to start its fintech activities and is looking for a payment gateway as a technical solution, including PSPs, ISOs, acquirers, integrators, fintech marketplaces, etc. Transferty experts are ready to develop extra features as well as special fintech solutions for your business to boost your payments

-

Which security standards does Transferty follow?

Trasferty is fully certified according to PCI DSS Level 1 standards. Our products are developed to prevent fraud and protect the data of our clients. We use tokenization, 3DS1 and 3DS2 flows, as well as roles and permissions managers, to reduce security risks and ensure the best performance of our solutions

-

How to contact us?

It is simple! You can contact us by filling out the contact form available on the Contact us webpage and providing the necessary information for us to address your query or concern

We strive to provide excellent customer service and aim to respond to your inquiries as quickly as possible. Please note that our response times may vary depending on the volume of inquiries, but we’ll make every effort to assist you in a timely manner

-

Can I try out Transferty’s payment gateway?

Absolutely! Transferty offers a three-month trial period, allowing you to process real traffic without incurring any Transferty commission. This trial period provides you with the opportunity to test and evaluate the advantages of Transferty’s solutions before making a commitment

-

How can my business get the individual offer for Transferty products?

We provide an individual approach for each customer, and for big players with significant payment volume and transaction numbers, we offer special conditions. To receive a personalized offer for Transferty products, fill out the form and specify your business requirements, and our sales team will review your request and provide you with a tailored offer that meets your needs

-

How can a payment gateway boost my payment conversion?

A payment gateway can significantly enhance your payment conversion in multiple ways:

- provides a wide range of payment methods, including alternative and local options, tailored to meet the diverse needs of your customers. This reduces cart abandonment and increases the likelihood of transaction completion

- offers advanced fraud prevention measures, such as customizable anti-fraud rules and 3D Secure authentication. The gateway allows flexibility in setting risk levels, minimizing false-positives and targeting only the riskiest transactions

- offers a user-friendly checkout experience with localized language options and adaptable design for various devices. Alternatively, merchants have the option to seamlessly integrate the payment gateway into their own checkout page. Both options contribute to improved conversion rates

- includes routing and cascading features that optimize transaction success rates. By automatically selecting the best acquiring bank or payment processor for each transaction, it reduces errors such as declines due to limits or provider issues, while also optimizing processing time

- provides real-time data and analytics on transaction performance, empowering you to quickly identify and address any issues. This enables you to optimize your payment flow, resolve bottlenecks, and continuously improve your payment conversion over time

-

Which factors can make my payment conversion decrease?

Several factors can impact your payment conversion, including a complicated checkout process, a lack of payment options, technical issues with the payment gateway, slow page load times, security concerns, and transaction errors such as errors from providers or exceeding MIDs limits. It’s important to regularly monitor and analyze your payment conversion rates to identify any issues and take appropriate actions to improve the user experience and optimize conversion rates

-

Why is payment conversion more critical than than revenue amount?

Payment conversion within a payment gateway refers to the percentage of successful transactions processed through the gateway. It is an essential metric for businesses that operate online and rely on electronic payments. While revenue is crucial for measuring overall financial success, payment conversion in a payment gateway holds its own significance for the following reasons:

1. Revenue realization: A high payment conversion rate in your payment gateway ensures that a larger percentage of your customers successfully complete their transactions. This directly translates into the realization of revenue for your business. Even if you generate substantial revenue, it is of little value if a significant number of transactions fail or are abandoned at the payment stage. Maximizing payment conversion ensures that you capture the full potential of your revenue2. Customer experience: The payment gateway is a critical touchpoint in the customer journey, as it’s where customers provide their payment information and complete their transactions. If the payment conversion rate is low, it may indicate issues or obstacles during the payment process that frustrate or discourage customers from completing their purchases. By prioritizing payment conversion, you focus on optimizing the customer experience and ensuring a smooth and seamless payment process, which can lead to higher customer satisfaction and repeat business

3. Operational efficiency: A high payment conversion rate within your payment gateway signifies that your payment infrastructure is functioning optimally. It suggests that the gateway is reliable, secure, and capable of processing transactions efficiently. Conversely, a low payment conversion rate may indicate technical issues, payment failures, or potential vulnerabilities in the payment process. By emphasizing payment conversion, you can identify and address any underlying issues promptly, ensuring the smooth operation of your payment gateway and minimizing revenue loss due to transaction failures

4. Fraud detection and prevention: Payment gateways are essential for optimizing fraud detection and prevention in transactions. By implementing advanced measures like customizable anti-fraud rules and 3D Secure authentication, payment gateways effectively mitigate the risks associated with fraud and chargebacks. The gateway allows flexibility in setting risk levels, minimizing false-positives and targeting only the riskiest transactions

While revenue is the ultimate goal, focusing on payment conversion within your payment gateway is critical for optimizing revenue realization, enhancing customer experience, maintaining operational efficiency, and mitigating fraud risks

-

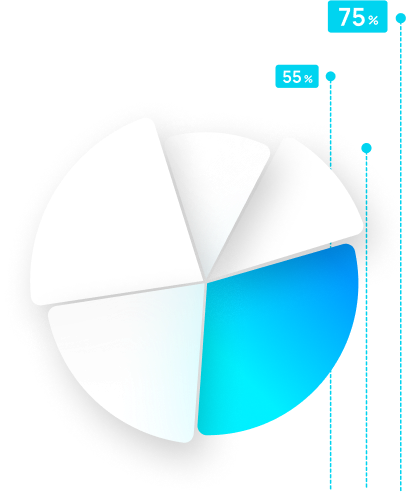

What is payment conversion?

Payment conversion refers to the percentage of successful transactions out of the total attempted transactions. In this context, it specifically pertains to the rate at which sales or transactions are completed.

For instance, let’s consider this example: There were 100 visitors, 20 of whom intended to make a purchase and proceeded to the checkout page. Out of those 20, 15 successfully completed their transactions, while the remaining 5 either abandoned the process, failed to pass the 3DS verification, or encountered some other error.

Thus, the payment conversion rate can be calculated as 15/20 = 0.75 = 75%. This indicates that 75% of the attempted transactions resulted in successful sales.

Simultaneously, the conversion rate of visitors to customers is 15%, as it represents the proportion of visitors who became paying customers

-

How many payment methods should I connect to increase revenue?

It depends on your business strategy, regions, customers, and sales channels. You may use as many payment methods as you need, and use other benefits of Transferty to boost your business

-

Why should I include alternative payment methods for the external markets?

Including alternative payment methods can help you reach a wider range of customers in different markets, especially in regions where credit card penetration may be lower. By offering local payment methods, you can provide a more seamless and convenient checkout experience for your customers, which can help increase conversions and customer satisfaction. Additionally, offering alternative payment methods can help you stand out from your competitors and build trust with your customers by demonstrating your commitment to serving their needs

-

Can I use both traditional and alternative payment methods in my payments?

Yes, it is common and beneficial to use both traditional and alternative payment methods in your payment options. By offering a combination of payment methods, you cater to a wider range of customer preferences and increase the likelihood of converting potential customers into paying customers. Transferty allows you to connect the payment methods you need to ensure your business’s growth

-

What is an APMs?

APMs stands for Alternative Payment Methods. These are payment options that differ from traditional payment methods such as credit cards, debit cards, or bank transfers. This term includes many payment methods, like e-money, cryptocurrency, and regional payment methods. APMs have gained popularity in recent years, driven by changing consumer behaviors, advancements in technology, and the desire for more convenient and flexible payment options

-

Can I set up an automatic currency conversion from the local currency?

Yes, a reliable payment gateway provider usually offers automatic currency conversion services that allow you to accept payments in multiple currencies and convert them to your local currency. This can be a convenient way to expand your business into different markets without having to manage multiple currency accounts

-

How can I integrate local payment methods?

We offer the flexibility to integrate any local or alternative payment method of your choice. Simply contact us, and we will work with you to ensure seamless integration into our payment gateway

-

Can I use the same payment gateway to expand my business into different markets?

You may be able to use the same payment gateway to expand your business into different markets. However, it’s important to ensure that the payment gateway supports the currencies and payment methods used in the markets you’re expanding into. Additionally, you may need to comply with local regulations and requirements, such as data privacy laws or anti-money laundering regulations, which could impact your choice of payment gateway. By choosing a payment gateway provider with local expertise, merchants receive easier and more organic expansion, which allows them to take advantage of their competitors

-

What kind of business will benefit from a high-risk payment gateway?

Businesses that may benefit from a high-risk payment gateway include those that operate in industries such as adult entertainment, online gambling, cryptocurrency, and certain types of e-commerce businesses that sell products with high chargeback rates, such as electronics or high-end luxury items. These businesses may find it difficult to secure payment processing services from traditional payment gateway providers due to their higher risk profile. A high-risk payment gateway can help these businesses accept electronic payments while minimizing their risk of chargebacks and fraud

-

How long does the integration take?

The amount of time it takes to integrate a payment gateway can vary depending on the complexity of the integration with the internal systems of a company. Some integrations can be completed in one week, while others may take several weeks or even a month. It’s best to consult with the payment gateway provider for an estimate on how long it will take for your specific needs and the technical characteristics of your business

-

Is a high-risk payment gateway safe?

Yes, a high-risk payment gateway is safe if it is provided by a reputable and reliable payment gateway provider. High-risk payment gateways are designed to handle transactions from industries or businesses that are considered high-risk due to factors such as high chargeback rates, potential fraud, or regulatory issues. These gateways are equipped with advanced security features, such as fraud detection and prevention tools, to help minimize the risk of fraudulent transactions.

-

What is a high risk payment gateway?

A high-risk payment gateway is a payment processing service designed specifically for businesses that are considered to be at a higher risk of chargebacks or fraud, such as adult entertainment, online gambling, or certain types of e-commerce businesses. These businesses typically have a higher risk of chargebacks due to the nature of their products or services, which can result in financial losses for the payment gateway provider

-

What is the difference between the high-risk payment gateway and the simple one?

What is the difference between the high-risk payment gateway and the simple one?

The main difference between a high-risk payment gateway and a standard or simple payment gateway is the level of risk associated with the business that is using the service. A high-risk payment gateway typically has stricter standards and more advanced fraud detection and prevention measures to protect both the merchant and the payment gateway provider. The specifics of a high-risk payment gateway is that such a provider has experience working with businesses, considered high-risk, understands the pain points of such businesses, and can easily remove the bottlenecks to ensure payment continuityThe main difference between a high-risk payment gateway and a simple payment gateway lies in the industries they cater to and the specific features and services they offer

Industries served: A simple payment gateway is designed to cater to a broad range of businesses across various industries, including low-risk and standard industries. It is suitable for businesses with relatively low risk of chargebacks, fraud, or legal and regulatory issues. On the other hand, a high-risk payment gateway is specialized for industries that are considered high risk, such as online gambling, adult entertainment, cryptocurrency, and others where there is a higher potential for fraud, chargebacks, or regulatory concerns

Compliance and legal support: High-risk payment gateways understand the unique legal and compliance requirements of high-risk industries

Expertise: The specifics of a high-risk payment gateway is that such a provider has experience working with businesses, considered high-risk, understands the pain points of such businesses, and can easily remove the bottlenecks to ensure payment continuity

-

How to choose a reliable high risk business payment gateway?

When choosing a high-risk payment gateway provider, it’s important to look for a provider that has experience working with businesses in your industry, as well as well-developed technology to provide reliable and secure payment processing services. It’s also important to look for a provider that offers flexible pricing options and high customer support

-

What are routing and cascading in payments?

Routing and cascading are two methods used in payment processing to ensure that transactions are processed efficiently and cost-effectively. Routing refers to the process of directing payment transactions to the most cost-effective payment processor based on factors such as transaction volume, currency, and location. Cascading, on the other hand, involves routing transactions to multiple payment processors in a predetermined order until a transaction is processed successfully. This can improve transaction success rates and reduce the risk of payment processing disruptions

-

Why is PCI DSS certification so important?

PCI DSS (Payment Card Industry Data Security Standard) certification is important because it ensures that your payment processing system is secure and compliant with industry standards. PCI DSS certification requires adherence to a set of security standards and practices designed to protect customer payment data from unauthorized access, use, or theft. Failure to comply with PCI DSS standards can result in significant fines and penalties and damage your business’s reputation

-

How much can the development of my own payment gateway cost?

The cost of developing your own payment gateway can vary widely, depending on the complexity of the solution and the level of customization required. It can range from tens of thousands of dollars to millions of dollars. In addition to development costs, there are ongoing maintenance and compliance costs associated with payment gateway solutions, including PCI DSS certification

-

How many acquirers is needed to ensure payment continuity?

It is recommended that merchants have at least two payment acquirers to ensure payment continuity. This is because if one acquirer experiences technical issues or service disruptions, the merchant can switch to the other acquirer to continue processing payments. Additionally, having multiple acquirers can provide redundancy and improve the reliability and speed of payment processing

-

What is a payment acquirer?

A payment acquirer, also known as an acquiring bank or acquiring processor, is a financial institution that processes payment transactions on behalf of merchants. They are responsible for authorizing and settling payment transactions with card networks such as Visa, Mastercard, or American Express, and ensuring that funds are transferred from the customer’s bank account to the merchant’s bank account

-

Why using a white-label payment gateway is better than developing my own solution?

Developing your own payment processing solution can be a time-consuming and costly process, requiring significant technical expertise and resources. In contrast, a white-label payment gateway offers a ready-made solution that can be customized and integrated into an existing platform more quickly and easily, allowing companies to focus on their core business. Additionally, a white-label payment gateway provider typically offers ongoing support and maintenance, as well as compliance with industry regulations and standards, reducing the risk and complexity of managing payment processing in-house

-

What kind of business will benefit from a white-label payment gateway?

Any business that wants to offer a seamless and fully branded payment experience for its customers can benefit from a white-label payment gateway. This includes online marketplaces, e-commerce platforms, software providers, and businesses that want to empower their brands, such as PSPs, banks, acquirers, ISOs, and big enterprises, among others

-

What’s the difference between a white-label payment gateway and a simple one?

A simple payment gateway typically provides a standard payment processing solution. In contrast, a white-label payment gateway offers a customizable solution that can be tailored to the specific needs and branding of a business. This includes custom branding, user interfaces, reporting, and integration options. With a white-label payment gateway, you can offer payment services to your customers under your own brand name

-

What is a white-label payment gateway?

A white-label payment gateway is a payment processing platform that can be rebranded and customized to match the branding of a specific company or organization. Essentially, it allows businesses to provide their own branded payment gateway to their customers without having to build the technology from scratch. This can help businesses improve their brand recognition and customer loyalty, as well as provide a seamless and cohesive payment experience for their customers. The white-label payment gateway can support a variety of payment methods, currencies, and languages and may also offer additional features such as fraud prevention, reporting, and analytics

-

Where are my reports stored?

All of your reports are easily accessible within your merchant account, specifically on the “Reports” page. From there, you can conveniently manage and filter data in order to generate reports based on your preferences. Additionally, there are no time frames for data storage, ensuring you have access to all relevant data

-

Can I share the access to report generation with my employees?

Yes, by managing the permissions, you can set the roles and permissions among your employees to different functions of Transferty, including report-generation tools

-

How can I tune the notifications in my merchant account?

To tune the notifications in your merchant account, you need to visit the Monitoring menu and set notification sending rules.

If you encounter any difficulties or have specific requirements, it’s recommended that you contact customer support for guidance on tuning the notifications in your specific account. Our support team is working 24/7 to help you with any questions you may have -

Why are notifications so important to keep payments ongoing?

Notifications are crucial for maintaining the continuity of payments by providing real-time updates, facilitating fraud detection and prevention, and supporting cash flow management. With the Transferty payment gateway, you have the opportunity to set your own rules using a variety of parameters such as card BIN, customer IP country, transaction status, payment method, provider, and many others. You can receive notifications each time a rule is triggered. Our notification system can help you receive only relevant updates on your payments via an endpoint or messenger, ensuring a quick response to any issues and increasing your revenue

-

Is it possible to send notifications to different employees of my company?

The notifications can be sent to the endpoints of your systems or to a messenger chat

-

Why is it important to analyze the payment process?

Analyzing the payment process in a payment gateway is important as it allows businesses to identify and address any inefficiencies, bottlenecks, or issues that may arise during payment transactions. It helps optimize the user experience by ensuring smooth and seamless payment flows, reducing friction, and minimizing errors. By conducting a thorough analysis, businesses can improve transaction success rates, enhance security measures, identify trends or patterns in payment behavior, and ultimately provide a more reliable and satisfying payment experience for customers

-

Why shall I include the local payment methods for the external markets?

Including local payment methods for external markets is important because it can help businesses increase sales and reduce cart abandonment rates in those markets. Customers in different regions have different preferences when it comes to payment methods and may be more likely to complete a transaction if their preferred payment method is available. By offering local payment methods, businesses can provide a more convenient and familiar checkout experience for customers and increase the likelihood of completing a sale

-

Why should I customize the receipts?

Customizing receipts is important because it can help improve the overall customer experience and provide important information to customers. Receipts can be customized with additional information about the purchase. Customizing receipts can help build customer loyalty, increase customer satisfaction, and provide customers with important information that they may need for future references, such as for tax or expense purposes

-

Why is it important to customize the checkout due to the customers’ specifics?

Customizing the checkout to meet the specific needs and preferences of customers is important because it can help improve the overall customer experience and increase sales. Customers have different preferences when it comes to payment methods and other aspects of the checkout process. By offering a customized checkout experience that meets these preferences, businesses can reduce cart abandonment rates, increase customer satisfaction, and build customer loyalty

-

How can event processing empower the security of payments?

Event processing enhances payment security by enabling real-time monitoring, rapid response to potential threats, and effective risk mitigation. It helps detect and address issues such as channel availability, faulty double funds debiting, fraud attempts, insufficient funds errors, provider problems, conversion deviations, and many others. By processing and analyzing these events promptly, businesses can take proactive measures to protect payment systems, prevent fraud, ensure compliance, and maintain a secure payment environment

-

Why is it important to analyze the payment process?

Analyzing the payment process in a payment gateway is important as it allows businesses to identify and address any inefficiencies, bottlenecks, or issues that may arise during payment transactions. It helps optimize the user experience by ensuring smooth and seamless payment flows, reducing friction, and minimizing errors. By conducting a thorough analysis, businesses can improve transaction success rates, enhance security measures, identify trends or patterns in payment behavior, and ultimately provide a more reliable and satisfying payment experience for customers

-

Why should I control and manage the limits?

Controlling and managing limits is important to ensure the continuity of payments. Limits can be set on a variety of parameters, such as transaction amount, frequency, and MID volume. By setting appropriate limits for specific MIDs, businesses can mitigate the risk of transaction failure and reduce the likelihood of payment declines due to rejection by the acquiring bank or PSP. As a result, the payment system will manage the payment flows accordingly and guarantee the efficiency and success of your transactions

-

Which limits can I set for my payments?

Basically, there are three categories in which you may set your payment limits: limits by MID, transaction limits, and card limits. In each category, you may set the appropriate minimum and maximum amounts, as well as time limits, for your transactions. These listed limits can be set per day and/or per month, giving you flexibility in customizing your payment restrictions

-

How to set the limits for my payments?

After signing up in the Transferty payment system, each merchant can adjust limits in Configuration Settings — Limits. That’s important to avoid unsuccessful transaction status because of reaching the limits. Limits setting allows you to reduce transaction processing time and increase conversion

-

How can I get a limits’ manager?

Each Transferty payment gateway user can easily utilize the limits’ manager to optimize the payments and improve the payment flow

-

What is a balance manager?

A balance manager is a functionality to help merchants manage their account balances. Firstly, it offers convenience by keeping them updated on the status of their balances in one centralized location, eliminating the need to check multiple platforms. Secondly, the ability to focus on specific balances through sorting and filtering options enhances their understanding of various processes and helps them prioritize tasks efficiently. Lastly, the balance manager allows merchants to easily manage multiple merchant accounts by organizing them based on merchant identification numbers (MIDs), currency, and provider, streamlining their operations and facilitating seamless account management

-

Who can see the changes in my merchant account?

Tracking changes made by employees in the payment system is crucial for maintaining control, detecting errors, preventing fraud, improving performance, ensuring compliance, and protecting against legal and financial liability. By closely monitoring and documenting these changes, businesses can identify and rectify errors, detect and investigate suspicious activities, provide necessary training and support, demonstrate compliance with regulations, and establish a clear audit trail for accountability and protection in case of disputes or legal inquiries

-

Why is it important to track the changes my employees make in the payment system?

Tracking changes made by employees in the payment system can help businesses maintain control and ensure that the system is being used appropriately. By monitoring changes, businesses can identify potential errors or fraud, and take action to correct them. Additionally, tracking changes can help businesses identify areas where employees may need additional training or support, and improve overall system performance. By maintaining a clear audit trail of changes, businesses can also demonstrate compliance with regulatory requirements and protect against legal or financial liability

-

How to use the Dispute Management tool?

Our Dispute Management tool centralizes disputes from multiple providers and acquiring banks, offering convenience. It provides details about disputed transactions, necessary documents, and enables merchants to submit proofs. We manage the process and keep you updated on outcomes, including wins, losses, or any additional steps required

-

How disputes manager can support my business?

The Transferty Dispute Management tool provides a solution to help your business manage disputes effectively. With our tool, you will be notified as soon as a dispute arrives, ensuring that you have enough time to take action and resolve the issue before it escalates. Our platform gathers all disputes in one place, regardless of how or which MIDs they arrive from, making it easy for you to track and manage them. You can also use filters to sort the disputes by ID, provider, category, status and more to resolve them appropriately. With our Dispute Management tool, you’ll be able to streamline your dispute resolution process, reduce your workload, and maintain customer satisfaction

-

What is a dispute?

A dispute refers to a disagreement or conflict between a customer (cardholder) and a merchant regarding a particular transaction. It typically arises when the customer questions or disputes the validity, accuracy, or quality of a purchase made using their payment card. Disputes can occur for various reasons, such as unauthorized transactions, billing errors, non-receipt of goods or services, dissatisfaction with the product or service, or issues related to refunds and returns. Resolving disputes involves investigating the claims, gathering evidence from both parties, and reaching a resolution that is fair and satisfactory for all parties involved. Dispute management processes and tools are used by payment service providers and merchants to handle and resolve these conflicts effectively.

-

What is BIN?

BIN stands for Bank Identification Number. It is the first 6–8 digits of a credit or debit card number and is used to identify the issuing bank and other information about the card, such as the card brand and card type (e.g., Visa, Mastercard, debit, credit). BIN information is often used by merchants and payment processors to verify card details and prevent fraud

-

Why is it important to analyze the payment process?

Analyzing the payment process in a payment gateway is important as it allows businesses to identify and address any inefficiencies, bottlenecks, or issues that may arise during payment transactions. It helps optimize the user experience by ensuring smooth and seamless payment flows, reducing friction, and minimizing errors. By conducting a thorough analysis, businesses can improve transaction success rates, enhance security measures, identify trends or patterns in payment behavior, and ultimately provide a more reliable and satisfying payment experience for customers

-

Is it possible to use auto-retry for different regions or alternative payment methods?

Yes, Transferty’s auto-retry feature is available globally and supports traditional and alternative payment methods to ensure the maximum growth of your business

-

What should I do to enable auto-retry?

The auto-retry feature is available for each merchant that uses Transferty Payment Gateway. You may tune the auto-retry instrument according to your business model by setting the auto-retry rules

-

What is auto-retry in payments?

Auto-retry in payments refers to a feature or functionality that automatically attempts to process a payment again if the initial transaction fails. When a payment fails due to reasons such as insufficient funds, technical issues, or connectivity problems, the auto-retry mechanism kicks in to automatically retry the payment without requiring manual intervention from the customer or the merchant. The system typically retries the payment using the same payment method and parameters as the initial attempt. Auto-retry aims to improve transaction success rates by providing additional opportunities for the payment to go through, increasing convenience for customers and reducing potential revenue loss for merchants

-

Is dynamic currency conversion obligatory for merchants or customers?

Dynamic currency conversion (DCC) is not obligatory for either merchants or customers. It is an optional service provided by some payment gateways. If you do not want to use it, the currency conversion may be performed by the rates of the acquirer you work with, or the purchase may happen in the currency you settle on as the main one

-

What are the advantages of dynamic currency conversion?

The lock of the exchange rate at the moment of purchase helps reduce the extra fees for customers

The conversion rate, price in the currency of the merchant, price in the currency of the customer, and fee are shown to the merchant in each converted transaction, which makes the process of dynamic currency conversion more transparent and clear -

What is dynamic currency conversion?

Dynamic currency conversion is a payment gateway feature that allows customers to pay for goods and services in their own currency, regardless of where the merchant is located or what currency the merchant accepts. This feature enables the payment gateway to automatically convert the transaction amount into the customer’s local currency at the time of payment, using the current exchange rate

Overall, dynamic currency conversion can provide merchants with a competitive edge in global markets, as it allows them to offer a more seamless payment experience for their customers while also generating additional revenue

-

How automatic currency conversion can benefit my business?

Automatic currency conversion can benefit your business by allowing you to expand your customer base and increase sales in foreign markets. By offering the ability to pay in local currency, you can make it easier for customers to understand the price of your products or services and avoid confusion or uncertainty caused by currency exchange rates. Additionally, automatic currency conversion can help reduce the risk of currency fluctuations and currency conversion fees, which can improve profitability and reduce costs. Overall, automatic currency conversion can help improve the customer experience and increase sales while also providing operational benefits for your business

-

Would tokens work if the customer’s card was replaced, renewed, or reissued?

No, in such a case, the customer should create a new token on the merchant’s platform

-

Are tokens vulnerable to cyberattacks?

To answer this question, we will explain step by step how tokenization works:

- The customer enters payment information on the merchant’s website or app

- The payment information is replaced with a unique token from the Transferty payment gateway

- The token is provided to the merchant for selling goods or services and to the acquirer bank for validation with Transferty payment gateway

- The transaction is then processed without using the customer’s payment information, after approval

The token is a meaningless string of characters that is of no use to hackers attempting to steal payment data or access the customer’s bank account. Therefore, even if hackers were to steal a token, they could not use it to withdraw money from the customer’s bank account or steal their payment data

-

Who can save cards?

Card data can be saved by various entities involved in the payment processing chain, such as card networks, card issuers, payment gateways, and other payment service providers. Transferty payment gateway do so in a secure way using technologies like tokenization and encryption. Tokenization replaces sensitive data with non-sensitive placeholders called tokens, while encryption transforms data into an unreadable format for confidentiality. Ultimately, it is the responsibility of merchants to ensure that their customers’ payment data is protected, and they should choose payment providers who prioritize data security and comply with industry standards such as PCI DSS

-

Why do merchants need tokenization?

Merchants need tokenization to reduce the risks of customer payment data leakage. Tokenization replaces sensitive payment information with a unique token that cannot be used by hackers to steal payment data. By removing payment data from their environment, merchants improve their security and reduce the reputational and financial risks associated with data leakage

-

Does card tokenization make the payment process more efficient?

Yes, card tokenization can make the payment process more efficient. When card tokenization is implemented, sensitive card data, such as the credit card number, is replaced with a unique token. The token can be used for future transactions without the need for the customer to re-enter their card information each time. This can reduce friction and speed up the checkout process, while also providing an additional layer of security

-

What is routing in payments?

Routing is a method used in payment processing to ensure that transactions are processed efficiently and cost-effectively. Routing refers to the process of directing payment transactions to the most cost-effective payment processor based on factors such as transaction volume, currency, location, and more

-

How to prevent payment gateway fraud?

Here are some methods that help prevent payment fraud:

3-D Secure (3DS2): A multifactor authentication for card payments is an effective tool, as it requires customers to verify themselves via phone or email

Card Verification Value (CVV): The CVV code is located on the back of a person’s credit or debit card and may be requested by the payment gateway to verify the customer

Fraud rules customization: The availability of setting the parameters that trigger actions to protect customers is an effective tool to reduce fraud. The merchant analyzes his clients and customizes the anti-fraud rules depending on the specificity of the audience he works with

-

How does payment gateway fraud happen?

The most common types of payment gateway fraud include:

BIN attacks and Card testing: In BIN attacks, cybercriminals use specialized software to generate long lists of potential card numbers by combining the first six digits of a card (the BIN) and testing them to find an active card that can be used for fraudulent purchases. In card testing, fraudsters create long lists of card numbers and make spam purchases in the hope that some of them will be successful

Theft of identity: By using identity theft tools, a hacker receives the personal payment data of a victim and makes a purchase using the victim’s card. To reduce the risk of data leakage, payment providers use tokenization technology, which replaces the customer’s sensitive data with a token, that could not be used by fraudsters to steal the information

To help prevent these types of fraud, payment providers often use various security measures, such as 3DS (3-Domain Secure), which adds an extra layer of authentication to the payment process by requiring the customer to enter a unique OTP (one-time password) or verification via a banking app before the transaction is approved. This security measure can help reduce the risks of payment gateway fraud and ensure that transactions are secure and protected

-

What is payment gateway fraud?

Payment gateway fraud refers to fraudulent activities or unauthorized transactions that occur within a payment gateway system. It involves the misuse of payment information or unauthorized access to payment accounts, resulting in financial loss for the merchant, payment processor, or the cardholder. Payment gateway fraud can take various forms, including stolen payment card details, identity theft, account takeover, fraudulent chargebacks, or manipulation of payment processes. Fraudsters may exploit vulnerabilities in the payment gateway system to gain unauthorized access, make fraudulent transactions, or deceive the system to bypass security measures. Choosing a reliable and secure payment gateway provider like Transferty is essential to protect against payment gateway fraud

-

What type of businesses will win, using recurring payments?

Subscription businesses

Businesses that sell subscriptions are the biggest beneficiaries of recurring payments due to their business model. It may be any streaming service, app, or software company

Membership businesses

Businesses that aim to sell customer membership usually charge a fixed price for their services or goods. For example, learning courses or fitness gyms

Businesses related to the financial sector

Financial services related to loans, insurance, investments, etc. They usually deal with fixed amounts, and they charge on a regular basis

-

Why are recurring payments so important for conversion increases?

Recurring payments, such as subscriptions or memberships, can provide a predictable revenue stream for businesses and encourage customer loyalty. By offering a recurring payment option, businesses can reduce the friction of having to repeatedly make payments for ongoing services or products, which can increase customer retention. Additionally, recurring payments can be a convenient way for customers to manage their budgets and ensure that they continue to receive the products or services they need without interruption

-

How do one-click payments improve sales?

One-click payments allow customers to complete their purchase with a single click without having to enter their payment and shipping information again. This can improve the customer experience by making the checkout process faster and more convenient, which can lead to increased sales. By reducing the number of steps required to make a purchase, one-click payments can also help reduce cart abandonment

-

What is API In online payments?

An API (Application Programming Interface) in the context of online payments refers to a communication interface that allows different systems to exchange information and interact with each other. When a merchant integrates with a payment gateway provider, such as our system, they typically connect to the provider’s API to enable the processing of transactions. An API enables merchants to securely and conveniently transmit payment data between their systems and the payment gateway provider. Our payment service offers a secure API to facilitate seamless integration and processing of online payments

-

What is H2H API?

H2H API refers to an integration method where two parties, a merchant and a payment gateway provider, exchange data directly through an API without the involvement of the end customer. In this case, the H2H API integration does not involve processing the card data directly by the payment gateway provider, nor does it require any interaction with the customer. Instead, the customer provides their card data to the merchant separately, outside of the payment gateway provider’s system. The merchant then sends the necessary card data to the payment gateway provider through the API, allowing for the secure and efficient processing of transactions. Note that in this case, the merchant must meet the PCI DSS requirements when working with this API, as it involves the transfer of sensitive card data

-

Why checkout customization could increase the number of sales?

Checkout customization can increase sales by improving the user experience, building trust, and enhancing branding. A streamlined and intuitive checkout process eliminates friction and makes it easier for customers to complete their purchase. Customized branding and design elements create a cohesive and professional impression, increasing trust and credibility. Security assurances and multiple payment options instill confidence. Ultimately, checkout customization helps create a positive and seamless buying experience, increasing the likelihood of conversions and driving more sales

-

How can I improve my online payments?

Provide multiple payment options: Offering a variety of payment options, such as credit/debit cards, digital wallets, and APMs, can help customers choose the method that is most convenient for them

Simplify the checkout process: Make the checkout process as simple and easy as possible, with minimal form fields and clear instructions

Ensure security: Choose a reputable payment gateway that has encryption and tokenization to protect sensitive customer information and increase trust

Enable one-click payments: Make the shopping process clear and fast for your customers to ensure more successful payments on your website

Enable recurring payments and a “save card” option: Build long-term relationships with your customers to increase their loyalty